Child Demat Account: Most Parents Save for Their Child's Future. Few Build Wealth This Way.

- Stay Informed With Sanil | Sanil Pinto

- 5 days ago

- 7 min read

Why More Parents Are Opening a Child Demat Account

Over the past few months, I noticed something interesting. Several parents—completely independent of one another—approached me with the same request.

"Can we open a Child Demat Account for our child?"

What surprised me wasn't the question. It was the age of the children. Some weren't even a year old. It made me realize this is a topic many more parents should understand.

Most parents start planning for their child's future almost from the day they are born. A savings account gets opened, a fixed deposit is created, an education plan is considered and, quite often, a child insurance policy is purchased. After all, every parent wants the same thing—to give their child opportunities they may not have had themselves.

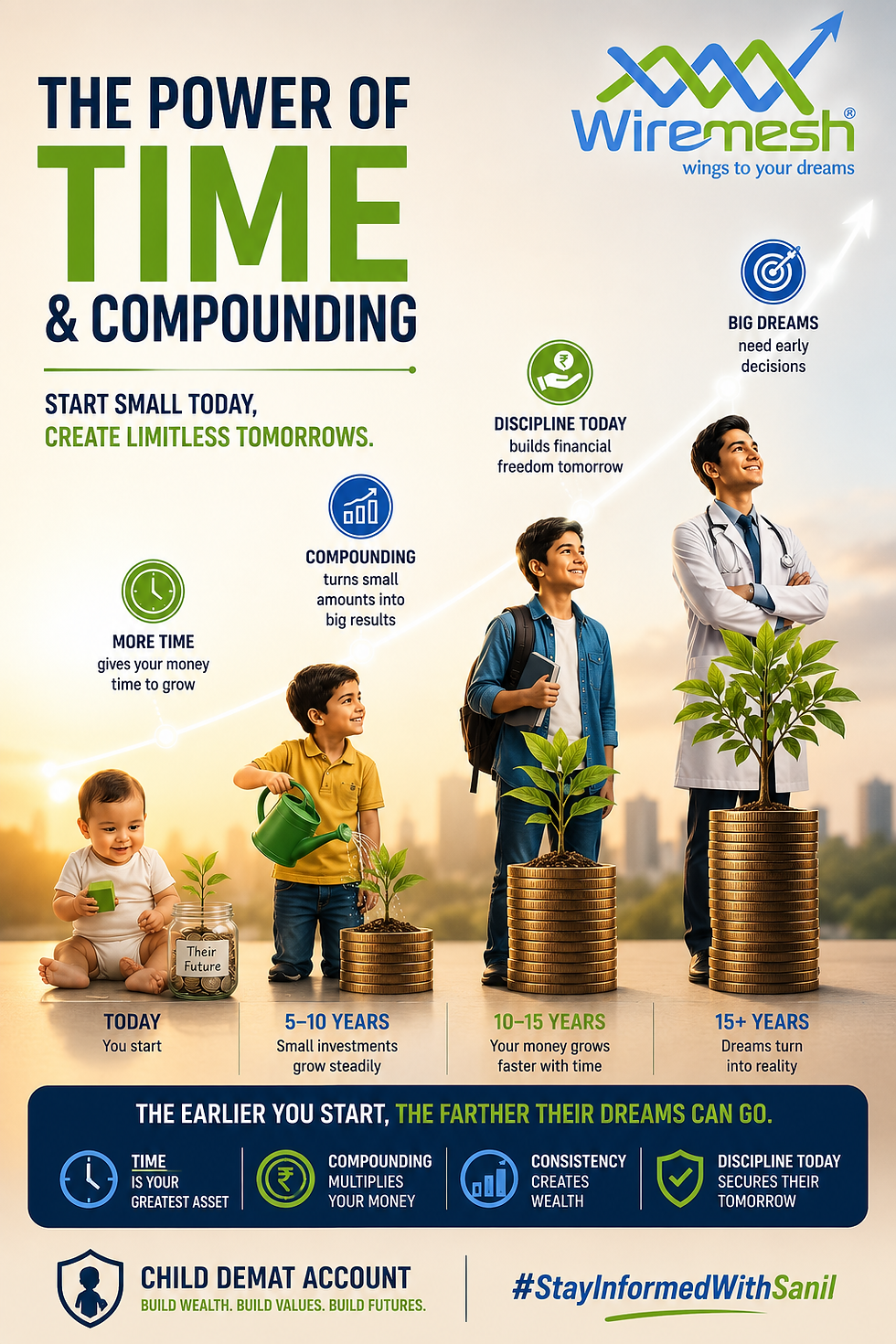

I've always believed that the earlier investing begins, the greater the opportunity for wealth to compound over time. A Child Demat Account simply takes that idea one step further.

At first glance, the concept may sound unusual. Why would a child who cannot walk, talk or understand money need a Demat Account? The answer is simple—they don't.

The parents do.

The objective isn't to create the next Warren Buffett or encourage children to track markets every day. It is to take advantage of something every child has in abundance and every adult wishes they had more of—time.

I've noticed that parents who open a Child Demat Account generally do so for one of two reasons. Some want to build a long-term investment corpus that could eventually help fund higher education, a first home, a business or simply give their child a financial head start. Others see it as an opportunity to teach their children how money works from an early age.

One client shared an approach that I found particularly interesting. Instead of allowing every birthday or festival gift to be spent immediately, a portion is invested. If grandparents gift ₹5,000 on a birthday, perhaps ₹2,000 or ₹3,000 is invested through the Child Demat Account.

As the years pass, something unexpected happens. The child becomes curious.

Why has one investment grown more than another? Why do markets sometimes fall? Why can't the money simply be withdrawn and spent today?

Without realizing it, they begin learning lessons about money that many adults never fully understand.

That is why I believe every parent should at least understand how a Child Demat Account works and whether it deserves a place in their family's financial plan.

Child Demat Account vs Child Insurance Plans: Which Makes More Sense?

If there is one financial product that has been marketed aggressively to parents over the years, it is the child insurance plan. The message is usually compelling. Secure your child's future. Guarantee your child's education. Ensure your child never has to compromise on their dreams.

As parents, it is completely natural to connect emotionally with these messages. The problem, however, is that emotional decisions do not always produce the best financial outcomes.

Over the years, I have met many parents who purchased child plans because they believed it was the responsible thing to do. What many didn't fully understand was how these products work, what they cost and how they compare with alternative approaches to long-term wealth creation. One of the biggest mistakes investors make is mixing insurance and investing. Insurance has a very important job. It protects your family financially if something unexpected happens.

Investing has a different job. It helps grow wealth over time. When the two are combined into a single product, the outcome is often a compromise. This is one of the reasons I generally prefer separating insurance from investing.

A Child Demat Account is not an investment product—it is an investment platform. Through it, parents can invest in mutual funds, ETFs and other SEBI-regulated investment options. Traditional child plans and ULIPs, on the other hand, operate within a different regulatory framework governed by IRDAI.

I am not suggesting that every child insurance plan is bad. I am simply suggesting that parents should understand exactly what they are buying before committing to a product that may remain part of their financial plan for nearly two decades. There is another reason I generally prefer investment-led solutions over most traditional child plans.

The data:

Over the last 15 to 20 years, diversified equity mutual funds have, in many cases, delivered returns that are significantly higher than traditional insurance-based savings products. That shouldn't be surprising. Traditional child plans are primarily designed to provide insurance with a savings component, whereas equity-oriented investments are designed to participate in the long-term growth of businesses and the economy.

Imagine two parents setting aside ₹10,000 every month for eighteen years.

One chooses a traditional child plan or ULIP. The other invests through mutual funds and other market-linked investments. Both want exactly the same outcome—a brighter future for their child. The difference is flexibility. Investment amounts can be increased, reduced or reallocated as family circumstances change. Goals evolve. Markets change. Children's aspirations change. The investment strategy can evolve too. Ultimately, the objective should not be to buy a product marketed for children. The objective should be to create the best possible financial outcome for the child. Insurance protects. Investments grow

A Child Demat Account Can Build More Than Just Wealth

One of the biggest advantages of a Child Demat Account has very little to do with the stock market itself.

It has everything to do with time.

Most investors understand the idea of compounding. What many underestimate is the impact of giving investments fifteen, eighteen or even twenty years to grow.

The good news is that parents don't need to begin with large amounts.

Some start by investing a monthly SIP.

Others simply invest part of the money children receive during birthdays, festivals and other special occasions.

The amount matters far less than the habit. Small investments made consistently over many years can become meaningful, not only because they compound but because they create an opportunity for children to learn alongside the investment.

As children grow older, they naturally become curious about why investments rise, why markets fall and why patience is often rewarded. Those conversations may ultimately prove more valuable than the investment itself. A Child Demat Account therefore serves two purposes. It helps build wealth for the future while helping children understand how wealth is created in the first place. Because while wealth can be inherited, good financial habits usually have to be learned.

How to Open a Child Demat Account in India

Opening a Child Demat Account is relatively straightforward.

Most investment platforms allow parents or legal guardians to open an account on behalf of a minor child. The account is operated by the parent or guardian until the child turns eighteen.

While requirements may differ slightly between institutions, you will typically need:

Child's PAN Card

Child's Aadhaar Card

Parent or Guardian's PAN Card

Parent or Guardian's Aadhaar Card

Bank Account Details

Birth Certificate (where required)

Once the account is opened, parents can begin investing based on their financial goals, investment horizon and risk appetite. Many families choose mutual funds and other SEBI-regulated investment options to gradually build wealth over time.

When the child turns eighteen, the account is converted into a regular account, allowing them to take ownership of a portfolio that may have been growing for many years.

Is a Child Demat Account Right for Your Family?

Like most financial decisions, there is no one-size-fits-all answer. However, I believe every parent should at least consider a Child Demat Account.

Not because it guarantees success. Not because it is the perfect solution for every family.

But because it offers something many traditional products struggle to provide—flexibility, transparency and the opportunity to harness the power of long-term compounding.

Whether your objective is creating an education corpus, giving your child a financial head start, teaching them how money works or simply putting birthday and festival gifts to better use, a Child Demat Account can become a valuable part of your family's financial plan.

After all, most parents spend years planning for their child's future. Perhaps the real question isn't whether your child needs a Child Demat Account. It is whether giving compounding a twenty-year head start could make a meaningful difference to the opportunities available to them later in life.

What Are Your Thoughts?

Have you considered opening a Child Demat Account for your child?

Would your objective be wealth creation, financial education—or both?

I'd love to hear your thoughts.

📩 Write to us at info@wiremeshin.com or visit wiremesh.com to be part of a growing community focused on practical, real-world financial decisions.

Stay Informed, Invest Wisely

ARN: 90622 | PMS: 201300009385 | RERA: A51700000493

About The Author:

Sanil Pinto - Stay Informed With Sanil

Take the first step in Giving Wings to Your Financial Dreams

Greetings, I'm Sanil — Founder of Wiremesh.

I started Wiremesh in 2010 to bring practical, insightful, and personalized financial advice to individuals and businesses. In 2018, Silicon India Magazine recognized our work by naming Wiremesh among the 10 Most Promising Investment Planning Companies.

Before founding Wiremesh, I worked with global BFSI leaders like HSBC and Barclays, where I led key business verticals and helped create substantial wealth across diverse portfolios.

Subscribe here to ‘Stay Informed With Sanil.’ If you're looking for expert-level market insights, smart investing strategies, and actionable financial tips—this is for you.

🔹 Thoughtful market commentary

🔹 Stock and sector insights

🔹 Strategic investment ideas

🔹 Real-world wealth-building guidance

Let’s turn your financial aspirations into action.

Disclaimer

This article is for informational purposes only and does not constitute investment advice. Investing in shares carries significant risk, including loss of capital, illiquidity, and valuation uncertainty. Readers are strongly encouraged to consult a SEBI-registered financial adviser before making any investment decisions. The information provided is based on publicly available data and sources believed to be reliable as of the date indicated, but may change without notice.

Open an Investment DMAT A/C catering to Mutual Funds, Stocks, Gold Bonds, NPS, and much more in easy steps

Comments